Tennessee's biggest health insurer helped insure its own financial health last year by rolling up record profits.

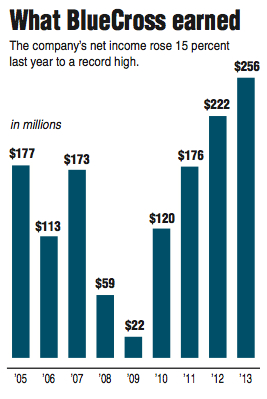

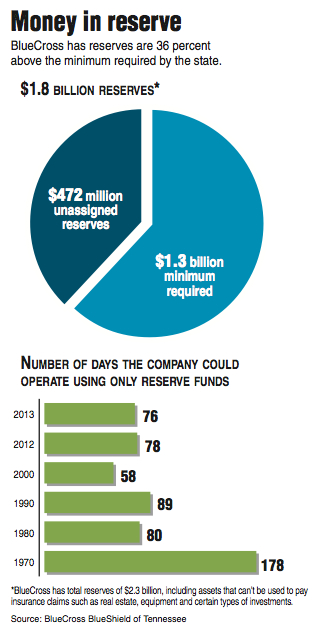

The not-for-profit BlueCross BlueShield of Tennessee boosted its net income in 2013 by 15 percent to a record high of $256 million. The income helped swell BlueCross total reserves at the end of 2013 to $2.3 billion, including $1.8 billion immediately available for paying claims -- more than 36 percent above the state-required minimum.

BlueCross officials say the extra income and reserves last year helped position the Chattanooga-based insurer for this year's challenging expansions under the new health care reform law.

"As a not-for-profit company, we've built up our reserves over 79 years to give us the capital for new initiatives and expansions to serve the market and to make sure we can weather unforeseen problems," BlueCross Vice President Roy Vaughn said.

BlueCross made money on both its commercial and government programs last year. BlueCross's subsidiary which handles the Tenn-Care program, Volunteer State Health Plan, earned $41.7 million, reversing losses the company had from its TennCare operations in previous years.

Five years ago in 2009, Volunteer State Health Plan reported a $95.6 million loss before the state revised the program and BlueCross restructured its operations to limit some of its costs.

BlueCross, which already insures 3.1 million Tennesseans, will pick up even more customers this year as the dominant player among the new health care exchanges offered in Tennessee. But the company's profits could be trimmed this year by higher taxes and lower margins on some operations as the new Affordable Care Act is implemented.

Profits uncertain for some in 2014

Most private health insurers boosted their earnings in 2013, but some firms have warned that profits could be hurt this year because of the costs of new individual customers signing up under the so-called ObamaCare provisions.

"There's a lot of uncertainty," Morningstar Research analyst Vishnu Lekraj said. "We haven't seen a whole quarter or two of claims activity from the exchanges. We don't know what's going to happen there."

BlueCross said last week it enrolled 133,291 Tennesseans through the government's HealthCare.gov website in the past six months. Many of those were previously uninsured, and the costs of such coverage for the new enrollees could be higher than for most individuals, at least initially, as customers go to doctors and detect previously unknown health problems.

Humana warned last week it expects lower income in 2014, in part, because of lower payments for Medicare Advantage under the new health reform law and because of potentially higher initial claims among those who previously didn't have health insurance and access to most doctors.

"There's still a lot of questions out there about what will happen with the Affordable Care Act, and I think that is causing a lot of concern not only with insurance companies but with businesses in general," said state Sen. Randy McNally, R-Oak Ridge, chairman of the Senate Finance Committee. "I've pushed for state government to have more in reserves, and I think with all of the uncertainty out there about health reform, if I was in the insurance business I would want to make sure I had sufficient reserves to see what was going to happen."

BlueCross says its reserves have grown along with its membership enrollment and were equal last year to what the company pays out in claims in 76 days, down from the 78-day cushion in the previous year.

Even supporters of the new health reform law said the strong fiscal health of BlueCross in Tennessee should help ensure that health plans remain strong and viable.

"This is a private market insurance system, so I'm glad to see that the companies that are involved are able to guard their assets," Walter Davis, executive director of the Tennessee Health Care Campaign. "It's good to see that people are participating in the exchanges at a higher level than some anticipated, and we appreciate that in some parts of Tennessee Blue-Cross is the only option for the new exchanges. I have no problem (with BlueCross's record earnings and reserves) as long as they are not cutting corners with service to their clients."

BlueCross is the only insurer to offer its individual health exchange policies in all 95 Tennessee counties. Among 54 new plans offered through the exchanges by BlueCross under the so-called ObamaCare, the most common offering by BlueCross of Tennessee was priced more than 40 percent below the U.S average.

City among 10 cheapest markets

A study by the Kaiser Family Foundation ranked Chattanooga and Knoxville among the 10 cheapest markets to purchase individual plans offered through the Affordable Care Act through the Tennessee BlueCross plan.

Henry Smith Sr., vice president of operations and chief marketing officer at BlueCross, said the company wanted to offer attractive plans and prices to help expand the number of Tennesseans with health insurance and thereby reduce the amount of indigent care costs shifted to other BlueCross commercial customers. Expanding health care coverage "is our mission," Smith said.

BlueCross said 91 percent of its customers maintained their health plans with BlueCross last year, one of the highest retention rates in the industry. Nationwide, BlueCross plans cover 85 percent of the Fortune 500 companies.

The Tennessee BlueCross plans include more than 25,000 providers across the state, or 90 percent of all doctors and specialists, although not all such providers are in every Blue-Cross plan.

"We offer a range of options for people to choose and where there are savings in some plans with more limited networks," Vaughn said.

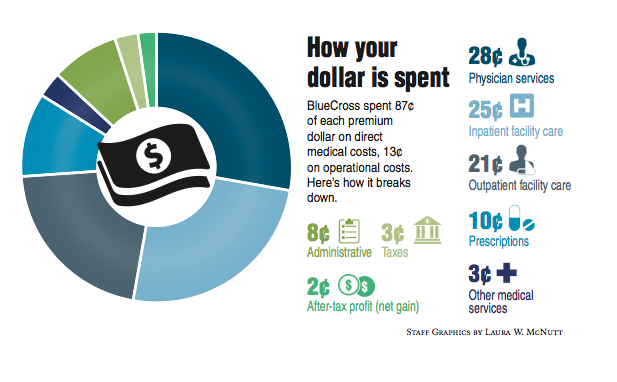

The new Affordable Care Act has capped the share of money insurers can keep in premiums to handle the costs of selling policies, processing claims, paying taxes and other administrative expenses incurred by the insurer. The new law requires insurers like BlueCross pay at least 80 percent of the premiums they collect from individuals or small employer groups -- and 85 percent of the premiums collected from large employer groups -- to hospitals, doctors or other health providers.

BlueCross of Tennessee generally stayed within the new law's guidelines last year. In 2013, BlueCross says it paid health care providers 88 percent of the premiums collected from large employers and 82 percent of the premiums collected from individual policy holders.

But for small employer groups of 50 or fewer employees, TVA fell just short of the requirement to pay at least 80 percent on premium income to providers. BlueCross paid 79.8 percent of the premiums it collected from small group employers for health care coverage last year. Company spokesperson Mary Danielson estimates making up for the shortfall is initially projected to mean a rebate of $1.6 million to be shared among the 13,800 small employer groups insured by BlueCross last year.

As part of what is not paid directly to doctors, hospitals, pharmacies and other providers by Blue-Cross, the company said it paid $270 million last year in local, state and federal taxes. The company said it also contributed $11.3 million to charitable projects across Tennessee that promote healthy living, health care access and quality of life.

BlueCross is the state's biggest nonprofit company with revenues of nearly $6 billion and 5,200 employees in five offices across Tennessee. But under the state legislation that created BlueCross in Tennessee in 1945, the company is taxed in the same manner as investor-owned insurance companies.

BlueCross profits are put back in the company or added to its reserves, Vaughn said.

CEOs rewarded for profits

The record earnings came in the first year that Bill Gracy was CEO of the company. For his performance, Gracy was paid $1.9 million as head of BlueCross in Tennessee in 2013. His predecessor, Vicky Gregg, was paid $5.1 million in her last year as CEO in 2012.

Gracy's compensation in his first year as CEO was only a fraction of that paid to some other health insurance executives.

Joseph Swedish, CEO of Wellpoint Inc., was paid nearly $17 million in total compensation last year; David Cordani, CEO of Cigna Corp., was paid $13.5 million last year, and Stephen Hemsley, CEO of UnitedHealthcare, was paid nearly $12.1 million in 2013.

Contact Dave Flessner at dflessner@timesfreepress.com or at 757-6340.