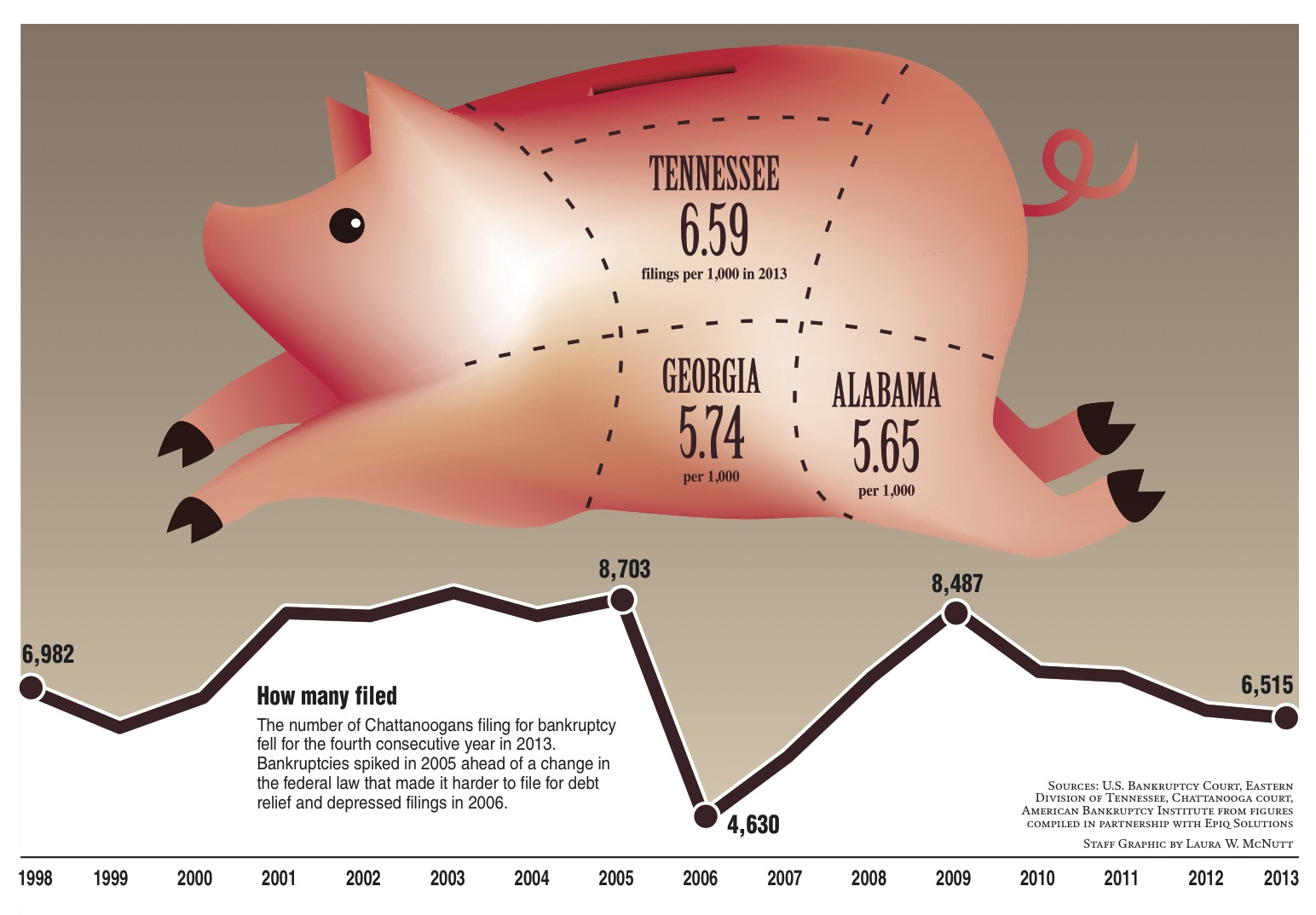

The number of Chattanoogans going broke or losing their properties to foreclosures declined last year, but Tennessee, Georgia and Alabama still led the nation in the rate of bankruptcies again in 2013.

Bankruptcy filings in Chattanooga fell last year for the fourth consecutive year since reaching a recession high in 2009, according to figures from the U.S. Bankruptcy Court. Last year, 6,515 consumers and businesses sought debt relief in bankruptcy court in Chattanooga, down 1.9 percent from the previous year and 23.3 percent below the level four years ago.

Property foreclosures in Hamilton County, which often lead individuals to seek bankruptcy protection to avoid, also declined another 15.3 percent in Hamilton County last year.

The drop in bankruptcy filings was even bigger nationwide. More than 1.03 American individuals and businesses filed for bankruptcy during 2013, but the total was down 13 percent from the previous year and the lowest total since 2007. Bankruptcy filings have declined steadily since 2010.

Experts say the drop in those seeking a fresh financial start through bankruptcy is due to historically low interest rates that have helped lower expenses for many debt-burdened Americans and greater credit restrictions on borrowing and filing costs on bankruptcies that have made it harder to get into financial trouble or to use the bankruptcy process for relief.

"Annual bankruptcy filings will likely continue to drop amid sustained low interest rates and high costs to file.," said Sam Gerdano, executive director for the American Bankruptcy Institute, the primary trade group that follows bankruptcy trends.

Fewer Chattanoogans also are seeking credit help than in the past. Consumer Credit Counseling Service in Chattanooga offered counseling to 293 individuals about possible bankruptcies last year, down from 429 the previous year, and CCCS aided another 98 clients with advice about home foreclosures, down from 208 in 2012.

"We're seeing a definite downward trend in the number of people we're seeing for foreclosure and bankruptcy problems," said LaTricia Schobert, executive director for Consumer Credit Counseling in Chattanooga. "Most of those facing foreclosures from the recession were already foreclosed upon and the CFPB (Consumer Finance Protection Board) is getting on mortgage companies now to make sure they have worked out every possible avenue to keep their clients in the home."

Schobert said most people are also more cautious with their money than before the recent recession and have limited their borrowing, at least to some extent.

"I think there has been a change in attitudes about money," she said. "More of the people we counsel now are coming to us because of life events like a death in the family, divorce or medical problem. Before a lot of people would come to us because they were overextended and simply had spent too much money."

Gerdano said bankruptcy filings could rise again as the economy improves, consumers borrow and spend more and lenders ease their credit requirements.

"Bankruptcy filings don't necessarily reflect how the economy overall is doing," he said. "Consumer spending drives 70 percent of the U.S. economy. As consumers and businesses are more confident about spending and take on more debt, the economy tends to grow faster but that also tends to lead more bankruptcies."

Conversely though, the improving economy also has helped inflate the value of most homes, which is the largest single asset for many Americans.

Regional differences

The per capita rate of those seeking any type of debt relief in bankruptcy court in Tennessee was more than twice the national average in 2013. Georgia and Alabama, respectively, were closely behind Tennessee with per capita filing rates in those states at least 70 percent above the U.S. average.

But the higher filing rate among Southerners doesn't necessarily mean more Tennesseans are dumping higher unpaid bills on to creditors by using the federal bankruptcy code for relief. A bigger share of those in bankruptcy in Tennessee, Georgia and Alabama file for debt reorganization and repay a bigger share of their debt through the bankruptcy court than in most of America.

Such debt reorganization plans under Chapter 13 of the federal bankruptcy code comprised nearly 58 percent of all bankruptcy filings in Chattanooga last year. Nationwide, only about 30 percent of all bankruptcies are Chapter 13 filings.

"The lawyers and judges in the South are more familiar and histrically have used Chapter 13 more often," Gerdano said.

Under a Chapter 13 plan, debtors pay back their debt over time under a court-supervised plan. Most bankruptcies nationwide are filed under Chapter 7 and involve a liquidation of assets to pay creditors.

"Chapter 13 plans tend to repay creditors more over time," Gerdano said.

Foreclosures fall

Another reason bankruptcy filings tend to be higher in the South is because such states usually make it easier than in other states for lenders to foreclose on delinquent debt on property, Gerdano said. To avoid such foreclosures, many people seek help with their debts in bankruptcy court. Many states require lenders to go to court and conduct a hearing before they can foreclose on a property, but Tennessee, Georgia and Alabama do not.

But the improving economy and tighter credit standards appear to be reducing foreclosure activity in nearly all states. In Hamilton County, the number of property foreclosures for all of 2013 totaled 952, down 15.3 percent from the 2012 total, according to filings with the Hamilton County Register of Deeds. The number of property foreclosures in Hamilton County during 2013 was the lowest since 2006.

Nationwide, CoreLogic reported last week that completed foreclosures nationwide in November were down 29 percent from the same time a year ago. Rising property values have both given debtors more equity and more reason to make their mortgage payments.

The improving economy also is cutting the number of business bankruptcies. Commercial filings during 2013 were down 24 percent from the previous year, according to nationwide figures compiled for the American Bankruptcy Institute by Epiq Systems.

Rob Jordan, a distressed credit analyst at Epiq, said low interest rates -- held down by the Federal Reserve Bank's easy monetary policy in recent years -- have allowed companies to refinance their debt and stay out of bankruptcy court.

"With interest rates low, companies that didn't previously have access to capital markets have access and are able to refinance their way out of trouble," he said.

Contact Dave Flessner at dflessner@timesfreepress.com or at 757-6340